Real Estate Investment in Greece: Tax Analysis for Israeli Investors

Real Estate Investment in Greece

A Tax Analysis of the Israeli Investor's Income Path

By David Melnik, Adv.

· · ·

Over the past decade, thousands of Israelis have acquired real property across Greece — in Athens, on the islands, and beyond. The market is one that recovered from the economic crisis that gripped Greece between 2010 and 2015. Even today, prices remain low relative to most of Western Europe, rental yields are attractive, the geographic proximity to Israel is convenient, the Golden Visa pathway is accessible — together creating a window of opportunity that thousands of Israeli investors have used.

However, the economic merit of such a transaction is not derived from gross yield alone. It depends on the tax holding structure through which the property is acquired. An Israeli investor acquiring property in Greece enters a dual-jurisdictional tax path — two systems of law, of two countries, coordinated between them through the tax treaty. Income flows from the Greek property to the Israeli owner, and each stage of the path is subject to a different legal regime. The choice between direct individual holding, holding through an Israeli company, or holding through a Greek company — determines the final effective tax rate that will reach the shareholder's pocket.

This article surveys, in brief, some of the available investment structures, tracing the income path from generation in Greece, through repatriation to Israel, and final distribution to the owner. The analysis is grounded in Israeli law, Greek law, and the bilateral tax treaty between the two countries.

The article focuses on the three basic holding structures. More sophisticated structures exist — such as a transparent Section 64 Company under the Israeli Income Tax Ordinance, or multi-tiered holding structures using conduit (PIPE) companies in intermediate jurisdictions such as Cyprus or the Netherlands. Such structures offer specific advantages in particular circumstances, but require detailed case-by-case analysis and are subject to additional constraints (including PPT tests and heightened economic substance requirements). They are not covered in this article.

The Israel-Greece Treaty as the Legal Framework

The Double Taxation Avoidance Treaty between Israel and Greece was signed on October 24, 1995, and entered into force on January 1, 1996. It determines which state has the authority to tax which income, and the allocation of income and credits between the two states. With respect to Greek real estate income held by an Israeli resident, two principal articles structure the picture.

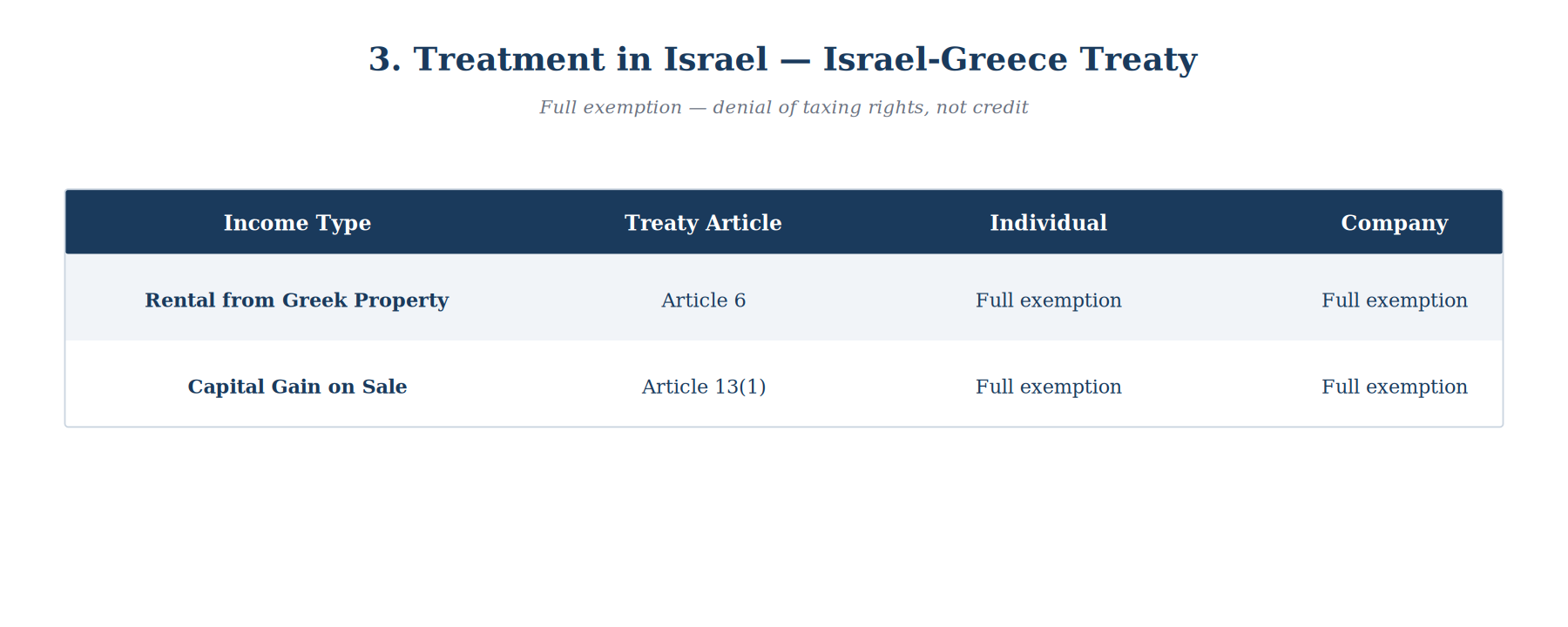

Article 6 of the treaty addresses income from immovable property, including rental income. The English text states "shall be taxable only in that other State" — granting exclusive taxing rights to the state in which the property is located. The Hebrew version, by contrast, grants Greece only primary taxing rights — wording that would theoretically preserve a residual taxing jurisdiction for Israel, subject to a foreign tax credit mechanism. Pursuant to the treaty itself, the English text governs in cases of conflict, and absent contrary judicial ruling, the practical result is that the income is not taxed in Israel.

Article 13(1) of the treaty parallels Article 6, but addresses capital gains from the disposition of the immovable property itself. Unlike Article 6, here the Hebrew and English texts are identical — both granting exclusive taxing rights to the state in which the property is located ("shall be taxable only"). There is no interpretive divergence here, and the Israeli exemption on capital gains from the disposition of Greek property is uncontested. An important point: Article 13(1) applies by its terms to any resident of a contracting state — individual or corporate alike. The exemption is not limited to individuals; an Israeli company disposing of Greek property also enjoys the same full exemption in Israel pursuant to this article.

The treaty was modified in 2021 through the OECD's Multilateral Instrument (MLI). Israel ratified the MLI on September 13, 2018, and Greece ratified on March 30, 2021. As a result, a Principal Purpose Test (PPT) was added to the treaty, under which treaty benefits will be denied where the principal purpose of an arrangement was to obtain those benefits. Genuine Greek real estate holding structures face no obstacle under the PPT — but documentation showing substantive business justification beyond tax savings is required.

Greek Taxation

Since the treaty grants Greece exclusive taxing rights over income from Greek real estate, Greece is the first (and effectively, the only) jurisdiction to impose tax on this income. Greek domestic law offers two parallel taxation paths — one for the individual holder, and one for the corporate holder.

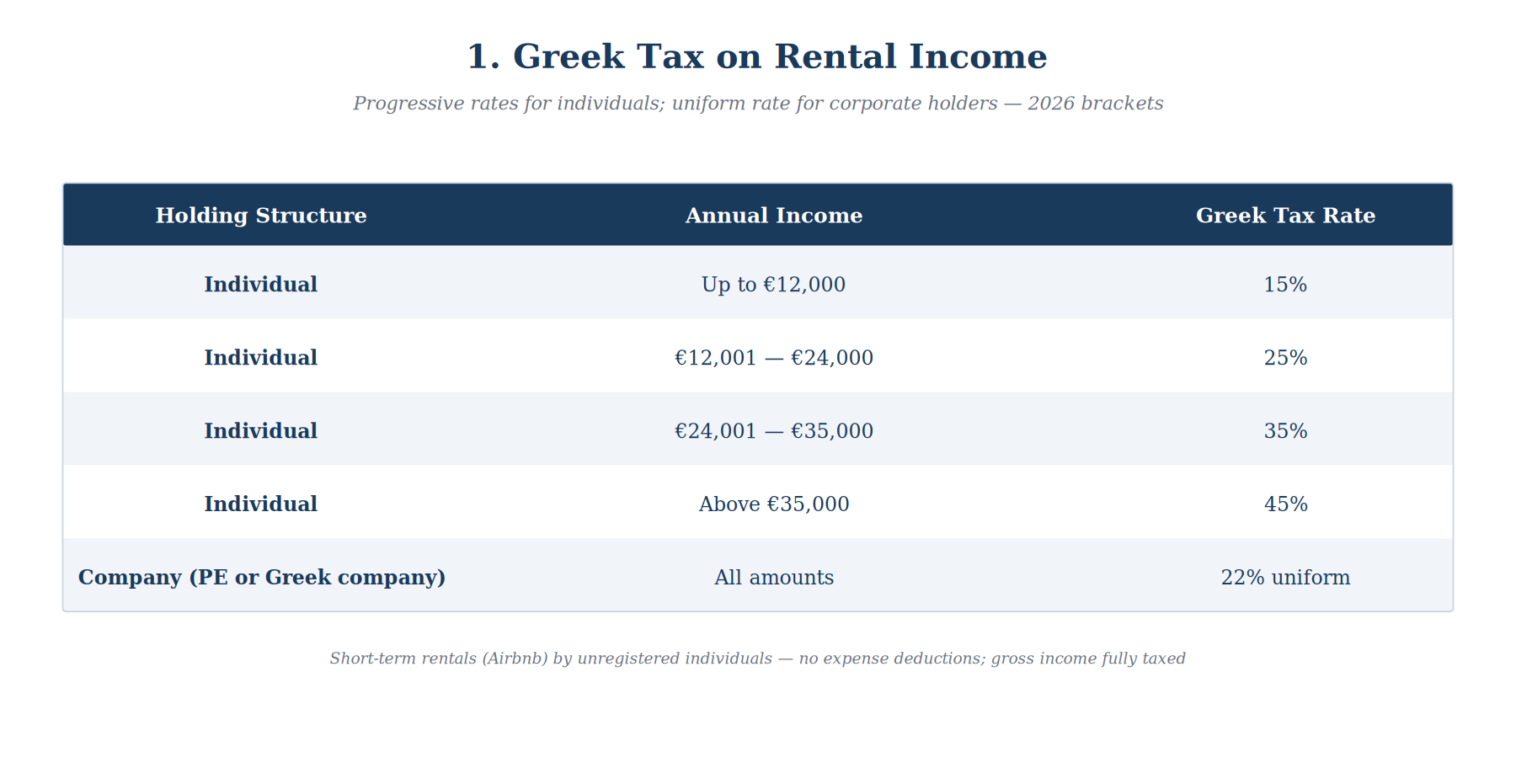

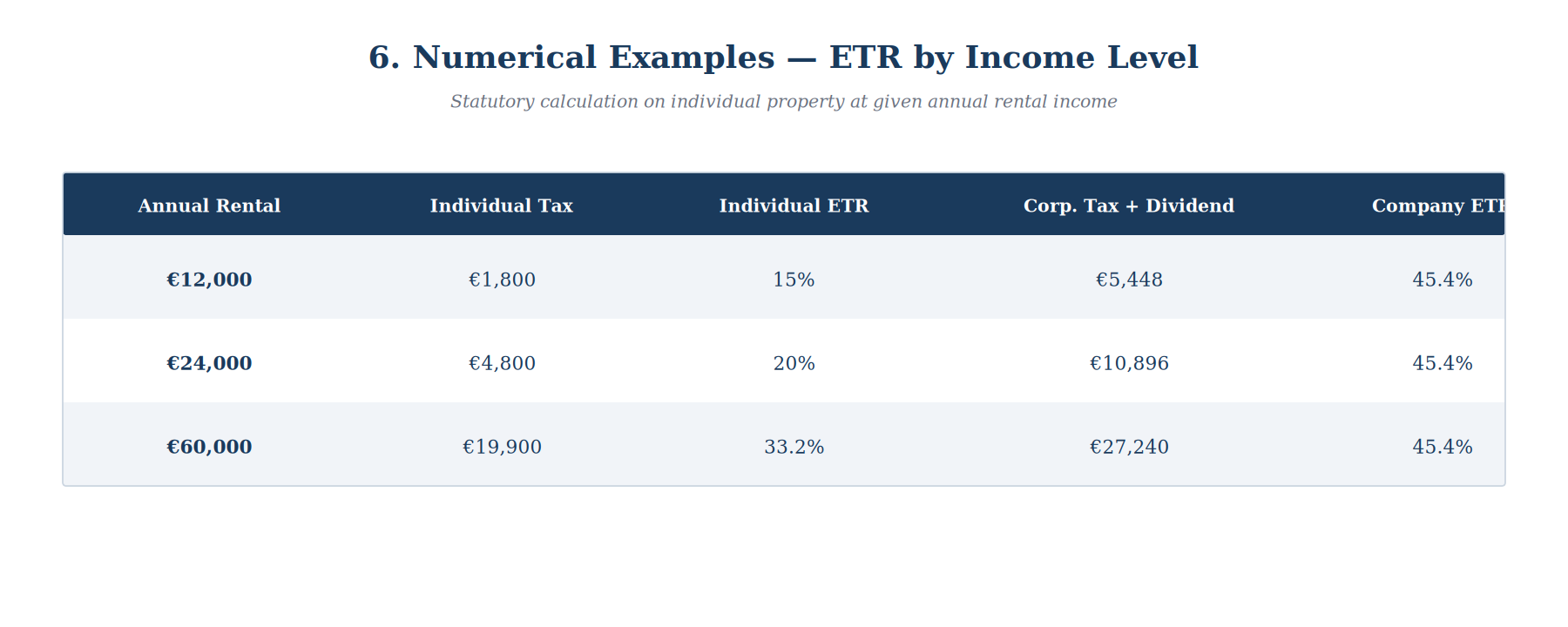

An Israeli resident individual holding Greek real estate is taxed on rental income at progressive rates, under brackets revised effective January 2026. Up to €12,000 in annual rental income — 15%. Between €12,001 and €24,000 — 25%. Between €24,001 and €35,000 — 35%. Above €35,000 — 45%. The law permits the deduction of certain operating expenses from taxable income — maintenance, property management, repairs, and a portion of utilities paid by the owner. In long-term rentals, gross income is reduced before tax is imposed.

The situation differs for short-term rentals (Airbnb). An individual not registered as a business operator may not deduct operating expenses or depreciation, and gross income is taxed in full at the progressive rates. Holding more than two properties in short-term rental requires registration as a business operator, which opens the possibility of expense deductions — but with additional procedural and tax obligations.

In the corporate path — whether an Israeli company holding through a Greek Permanent Establishment (PE), or a Greek company — the Greek tax rate is uniform: 22% corporate income tax, regardless of income level. This rate has been in effect since 2022 and is not graduated. At the corporate level, full deduction is permitted for operating expenses, depreciation on the property, and interest expenses — subject to the Greek thin-capitalization rules adopted pursuant to the EU ATAD Directive, under which interest deductibility is capped at 30% of EBITDA, with a €3 million safe harbor. The relatively broad scope of deductible expenses at the corporate level materially reduces the Greek taxable base, so that the 22% statutory rate translates in practice to a lower effective rate.

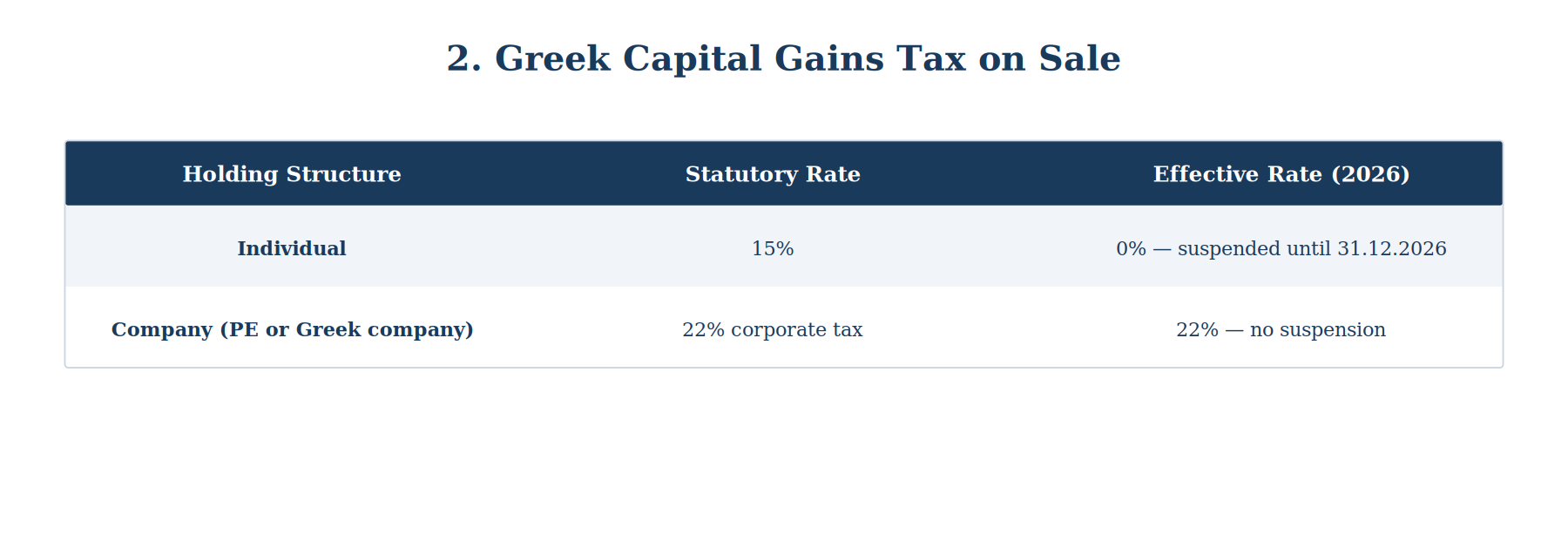

Capital gains from the disposition of the property are bifurcated by the nature of the holder. For an individual, the Greek tax rate is 15%, however it is currently suspended in practice through December 31, 2026. During the suspension period, an individual selling Greek property pays no capital gains tax in Greece. For a corporate holder, the gain is incorporated into the regular corporate tax framework — 22% — and the suspension does not apply.

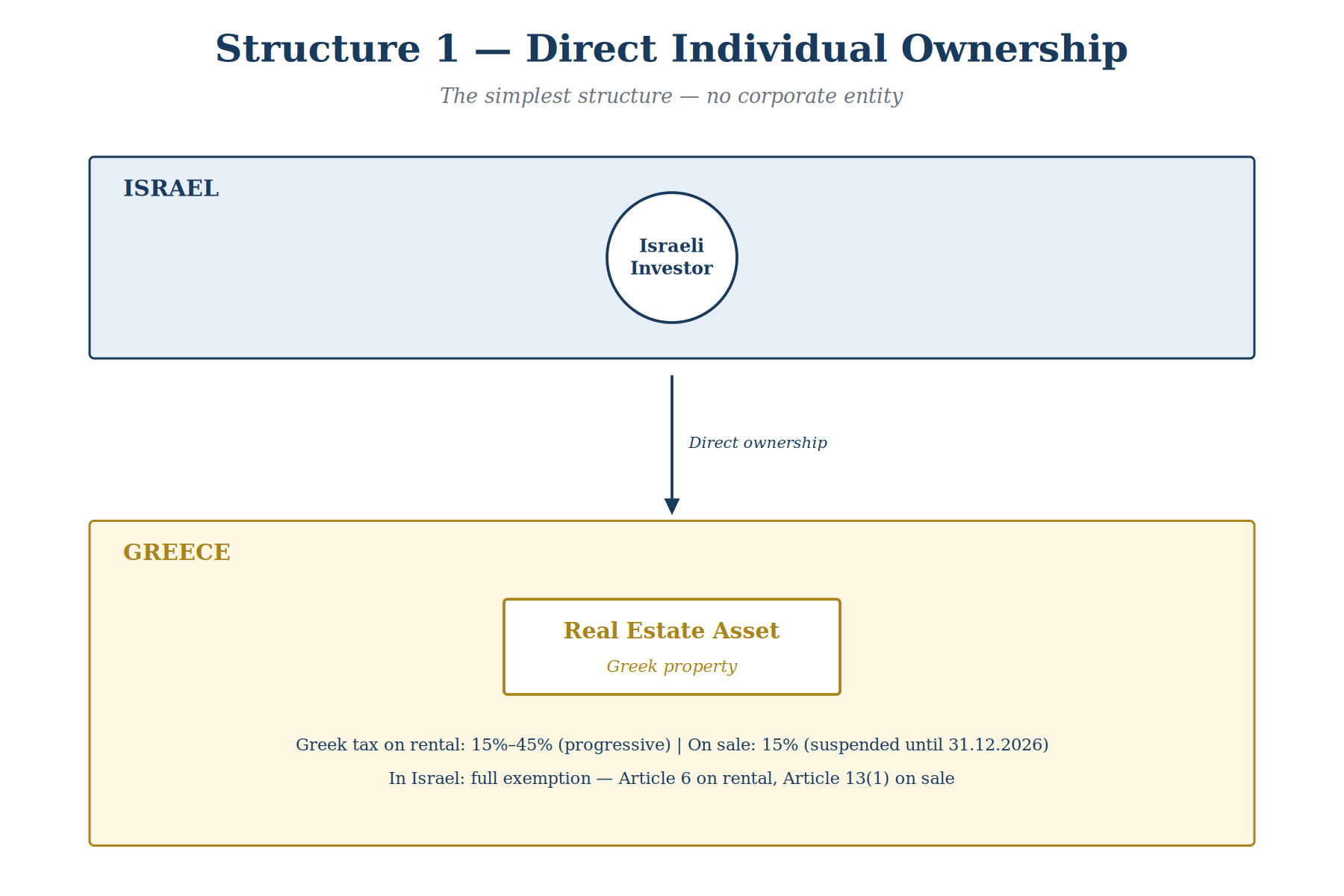

The Israeli Path — Direct Individual Ownership

The simplest structure is for the Israeli investor to hold the Greek property in his own name, without any intermediating corporate entity. He registers the property in his name with the Greek land registry and receives the rental income directly into his account. When the day of sale arrives, the proceeds flow directly to him. The diagram below illustrates the structure:

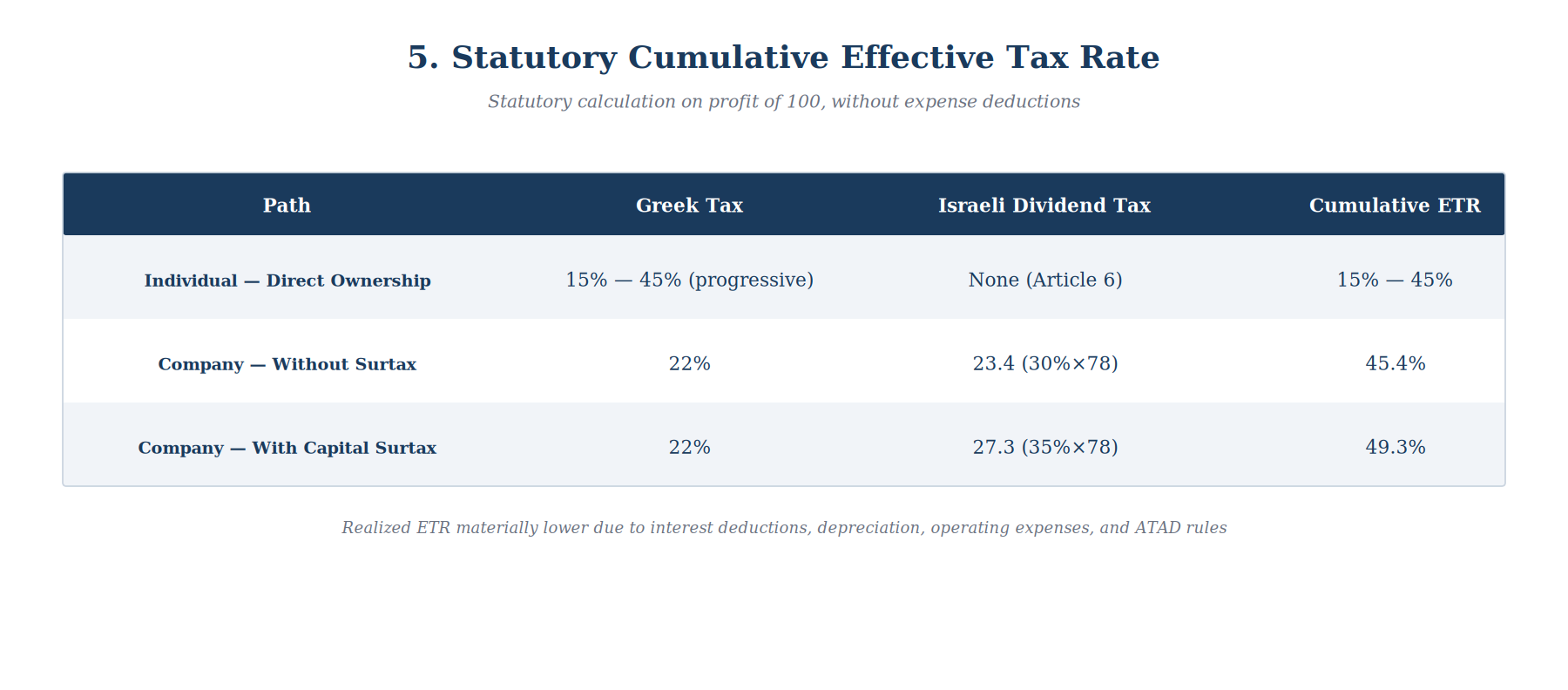

In this path, no additional tax layer is imposed beyond the Greek tax. Article 6 of the treaty provides full exemption in Israel on rental income, and Article 13(1) provides full exemption in Israel on capital gains from disposition. The final effective tax rate equals the Greek tax alone — 15% to 45% on rental income depending on the level of income, and zero on disposition during the suspension period.

An additional advantage lies in the absence of complexity. There is no need to establish a company, no corporate filings, no director appointments, and no corporate law obligations. The principal disadvantage is personal exposure of the investor — any legal dispute concerning the property is transmitted directly to him, without the protective veil of a separate legal entity.

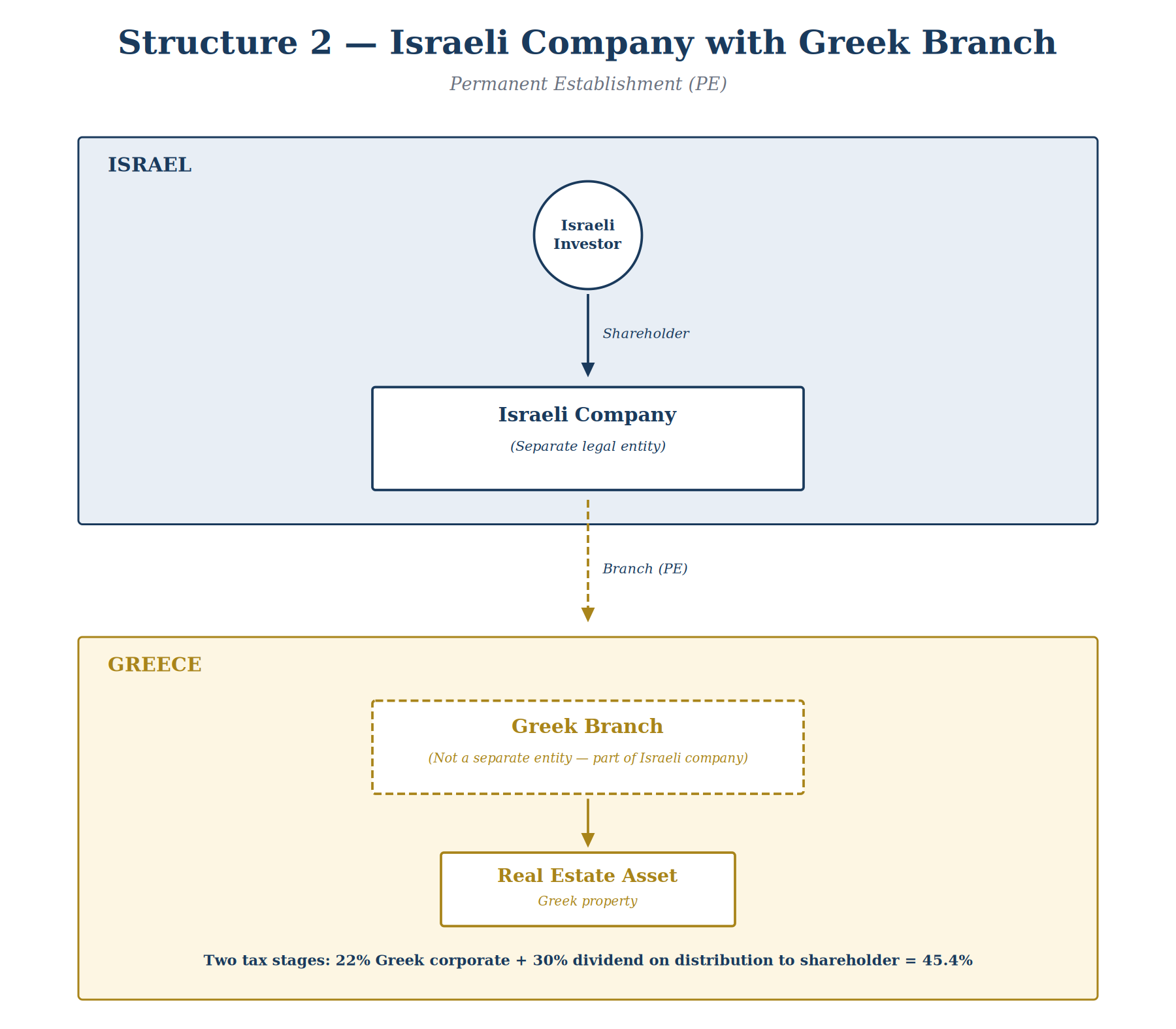

The Israeli Path — Israeli Company with Greek Permanent Establishment

An alternative structure is to hold the property through an Israeli company that establishes a branch in Greece (a Permanent Establishment, or PE) for purposes of holding the property. The Greek branch is not a separate legal entity — it is part of the Israeli company — but international tax law treats it for tax purposes as a separate unit generating income in Greece. The diagram below illustrates the structure:

In this structure, the income generated at the branch level is taxed in Greece at 22% corporate income tax. The branch pays no additional branch tax (Greece does not impose a Branch Profits Tax), and the profit flows to the Israeli company fully exempt under Article 6 of the treaty. At the Israeli company level — zero Israeli tax. Up to this point, the result is substantively identical to that of an individual: Greek tax only, zero Israeli tax.

The material difference emerges at the next stage. In the individual structure, the income is already in the owner's pocket. In the corporate structure, it sits in the company's treasury — not in the shareholder's pocket. The company is a legal entity separate from its shareholder, and therefore transferring the funds to him requires an additional mechanism: a dividend distribution. The corporate mechanism produces two tax stages. The first stage, at the corporate level, has been exhausted (22% in Greece, zero in Israel). The second stage, at the shareholder level, materializes upon dividend distribution.

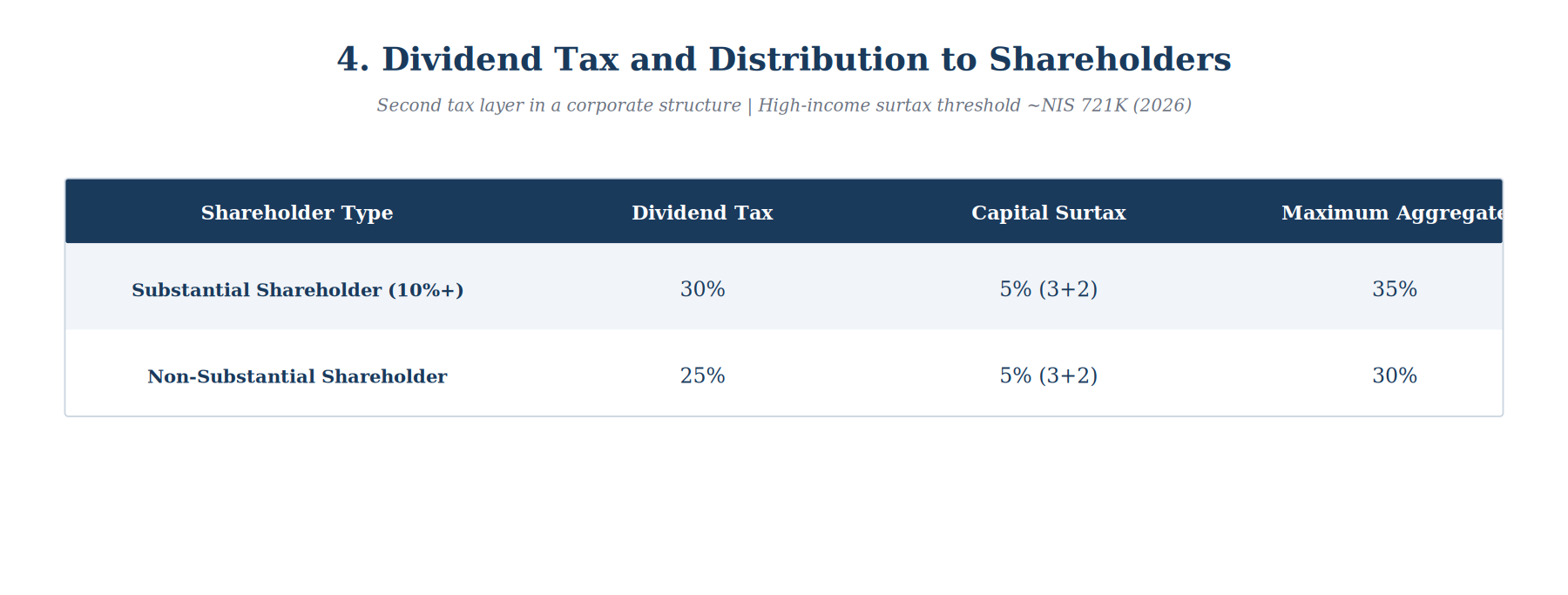

The dividend tax rate applicable to a substantial shareholder (10% holding and above) is 30%, applied to the distributed amount. Dividends are capital income, and therefore an individual whose total annual income crosses the Israeli high-income surtax threshold (approximately NIS 721,000 in 2026) is also subject to a capital surtax at an aggregate rate of 5% — composed of a 3% base surtax plus an additional 2% capital surtax — on capital income exceeding the threshold.

A statutory calculation on a profit of 100 yields 22% Greek tax + 30% dividend on the remainder (78) = 45.4%. With the capital surtax, the figure rises to 49.3%. However, this is a calculation on profit, not on gross income, and is also predicated on the assumption that no financing expenses, depreciation, or operating expenses are deductible at the corporate level. In practice, real estate investments are typically leveraged, depreciation is deductible over time, and management and operating expenses exist — all of which reduce the Greek taxable base, so that the actual realized ETR is materially below the statutory figure. In investments with reasonable leverage, the realized ETR may be significantly lower.

Prior to the 2024 amendment, it was possible to defer the dividend layer by retaining earnings within the company without distribution. The 2024 amendment, which took effect on December 31, 2024, applies to closely-held companies (five or fewer shareholders) and imposes an annual 2% tax on undistributed retained earnings, unless an annual distribution of 5% of total undistributed earnings is made. Earnings attributed to the Greek branch are also included in the calculation — there is no geographic shelter, as they are recorded on the books of the Israeli company in the year in which they arise. The classic deferral of the dividend layer has been substantially curtailed.

Structural Advantages of Corporate Holding

Beyond the pure tax consideration, a corporate structure offers three structural advantages that do not depend on the tax rate.

The first is the ability to reinvest within the company. In the individual structure, all income from the property reaches the owner after payment of Greek tax, and any reinvestment is made from funds that have already passed through the full taxation stage. In the corporate structure, the company may retain its earnings after payment of the 22% Greek tax and reinvest them — to acquire additional property, to expand operations — without crossing the dividend layer. The 2024 amendment to the Trapped Earnings Tax narrows this advantage by mandating an annual distribution of 5% of accumulated earnings, but does not eliminate it entirely; a meaningful portion of earnings may remain within the company to be used for additional investments.

The second is limited liability. In the individual structure, any legal dispute concerning the Greek property — tenant claims, regulatory issues, liabilities arising from management contracts — is transmitted directly to the investor, and may compromise his other assets. In the corporate structure, exposure is limited to the assets of the company alone, providing a genuine separation between the specific Greek property and the rest of the investor's wealth.

The third is flexibility in ownership structure. When an investor wishes to add partners, transfer a portion of the rights to family members, or combine multiple investors in a single project, a corporate structure permits this through internal share allocation — without requiring changes to the Greek land registry, without the tax implications of real estate transfers, and without the legal entanglement of joint ownership in a single property. This is a material advantage for family planning and for investment partnership structures.

The Israeli Path — Greek Company Owned by an Israeli Resident

A further option is to establish a Greek tax resident company that holds the property. The Greek tax rate is identical to that of an Israeli company with a Greek branch — 22% uniform corporate tax. The diagram below illustrates the structure:

The first principal issue in this structure does not lie in Greece but in Israel. Section 1 of the Israeli Income Tax Ordinance provides that a company is an Israeli resident if its control and management are exercised from Israel. A Greek company whose board meets in Israel, whose CEO is based in Israel, and whose substantive business decisions are made from Israel — is deemed an Israeli resident in every respect, notwithstanding its Greek incorporation. Where dual residency exists, the treaty resolves it by reference to the place of effective management — which is Israel. The practical consequence in such a case is that the Greek company behaves, for Israeli tax purposes, as an Israeli company; the Trapped Earnings Tax applies to it; and the theoretical advantage of the structure is eliminated.

A second issue requiring examination is the Controlled Foreign Corporation (CFC) provisions of Section 75B of the Israeli Income Tax Ordinance. This section applies where three cumulative conditions are met: first, more than 50% of the means of control of the foreign company are held by Israeli residents; second, the majority of the company's income is passive (including rent, interest, dividends, and capital gains); third, the tax rate in the state of incorporation on such passive income is below 15%. If all three conditions are met, the foreign company's income is deemed distributed to the Israeli individual as a constructive dividend — even where no actual distribution occurred — and tax is imposed in Israel.

In the case of a Greek company holding Greek real estate, it is reasonable to assume that the CFC provisions will not apply, since the Greek tax rate on the relevant income (22%) exceeds the 15% threshold specified in the section. However, case-specific examination is required: first, whether the Israeli shareholders indeed hold more than 50%; second, whether the effective rate actually paid in Greece (after deductions) does not fall below 15%; third, if the income includes various components (such as rental income on the one hand and capital gains on the other), each component must be examined separately.

A third issue is the PPT — the Principal Purpose Test added to the treaty through the MLI. Establishing a Greek company to hold Greek real estate by an Israeli resident, without substantive business justification beyond tax savings, is exposed to a claim that the principal purpose of the arrangement is to obtain a treaty benefit. The Israeli tax authority may argue that there is no justification for a Greek company in lieu of direct holding or holding through a branch of an Israeli company.

From a practical standpoint, a Greek company structure stands only where control and management are exercised in practice from Greece — which requires genuine Greek economic substance: a professional Greek director, an actual office in Athens, business decisions made in Greece, and minutes kept in Greek. Annual maintenance costs for such a structure range from €10,000 to €20,000.

Actual Effective Tax Rate

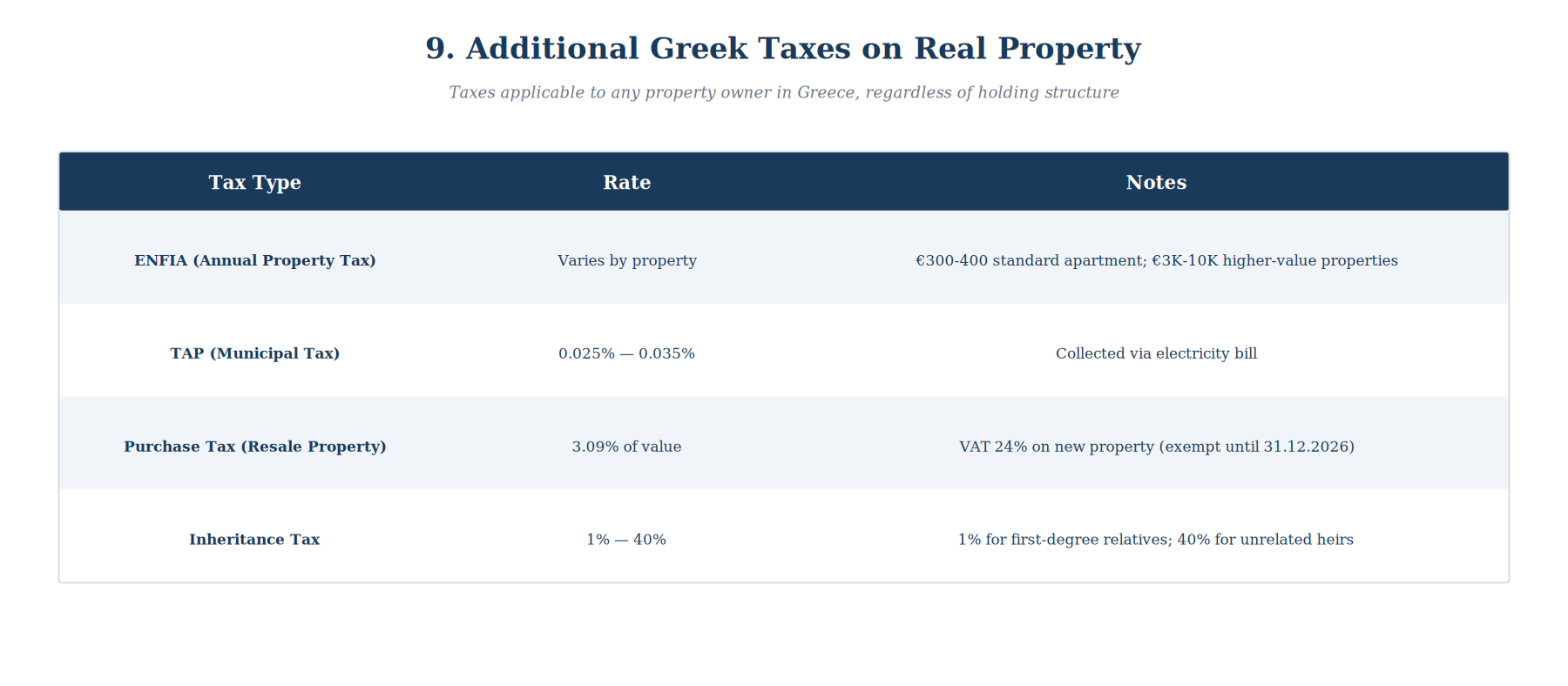

A statutory ETR calculation on a profit of 100 — 22% corporate tax plus 30% dividend on the remainder — yields a theoretical figure of 45.4%, rising to 49.3% with the capital surtax. This is a calculation on pure profit, without expenses, without depreciation, and without leverage. In practice, the reality is different. Most real estate investments are subject to some leverage, depreciation on the property is deductible over a defined useful life, and ongoing operating expenses exist — maintenance, management, insurance, local taxes, and the Greek ENFIA property tax. All of these reduce the taxable base in Greece before tax is imposed.

In realistic investment structures, particularly those benefiting from bank financing, the realized ETR is materially below the statutory rate. When comparing an individual structure to a corporate structure, the realized differential between the two depends on numerous variables — the scope of deductible expenses, the level of leverage, the income level relative to the Greek tax brackets, and others. In significantly leveraged investments, the corporate structure can offer a realized ETR materially superior to that of the individual structure.

Factors Guiding Structure Selection

The choice of structure is not uniform. It derives from a number of variables, each of which moves the equation in a different direction. The principal factor is the scale of activity. A single property generating moderate rental income — an individual structure is simple and tax-efficient. A portfolio of multiple properties with substantial cash flow — the management costs of corporate structures begin to be justified by the management and flexibility advantages they provide.

Financial strategy is also a decisive variable. Drawing current cash flow to the owner eliminates part of the advantage of a corporate structure, since each distribution immediately triggers the dividend layer. Long-term capital building justifies corporate structures particularly where reinvestment within the company is feasible — but the Trapped Earnings Tax limits this opportunity, since it mandates an annual distribution of 5% of accumulated earnings, or a 2% penalty tax.

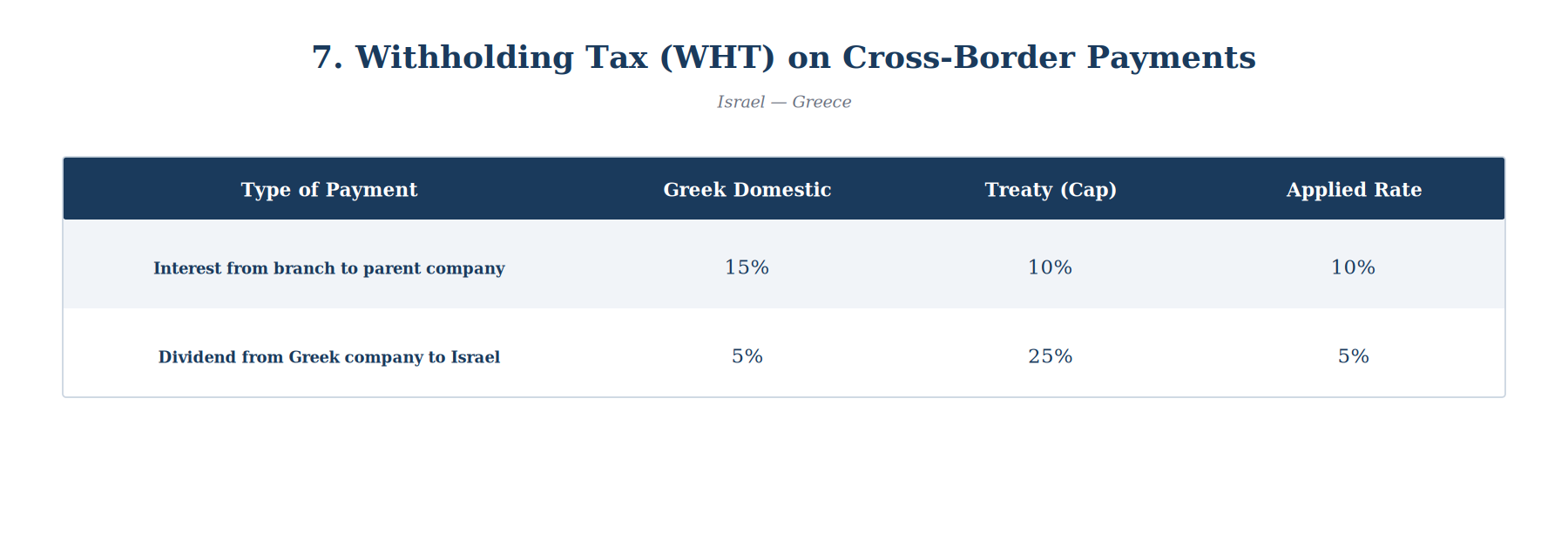

Leverage levels can tilt the balance in favor of a corporate structure. An investment funded by significant debt justifies structures that enable the creation of deductible interest expenses in Greece, and intercompany loan structures between the Israeli company and the Greek branch generate Greek tax savings. An additional point worth noting: interest paid by the branch to the Israeli company is subject to a 10% withholding tax under the treaty (the Greek domestic rate is 15%, but is capped at 10% under the treaty). Sophisticated financing structures can materially reduce the realized ETR.

Intergenerational transfer planning is also a relevant consideration. Greek inheritance tax ranges from 1% for first-degree relatives to up to 40% for strangers. In Israel, there is no inheritance tax, but the Greek property remains subject to Greek law upon transfer, regardless of the holding structure. If the heirs are not close family members, advance planning has material tax significance.

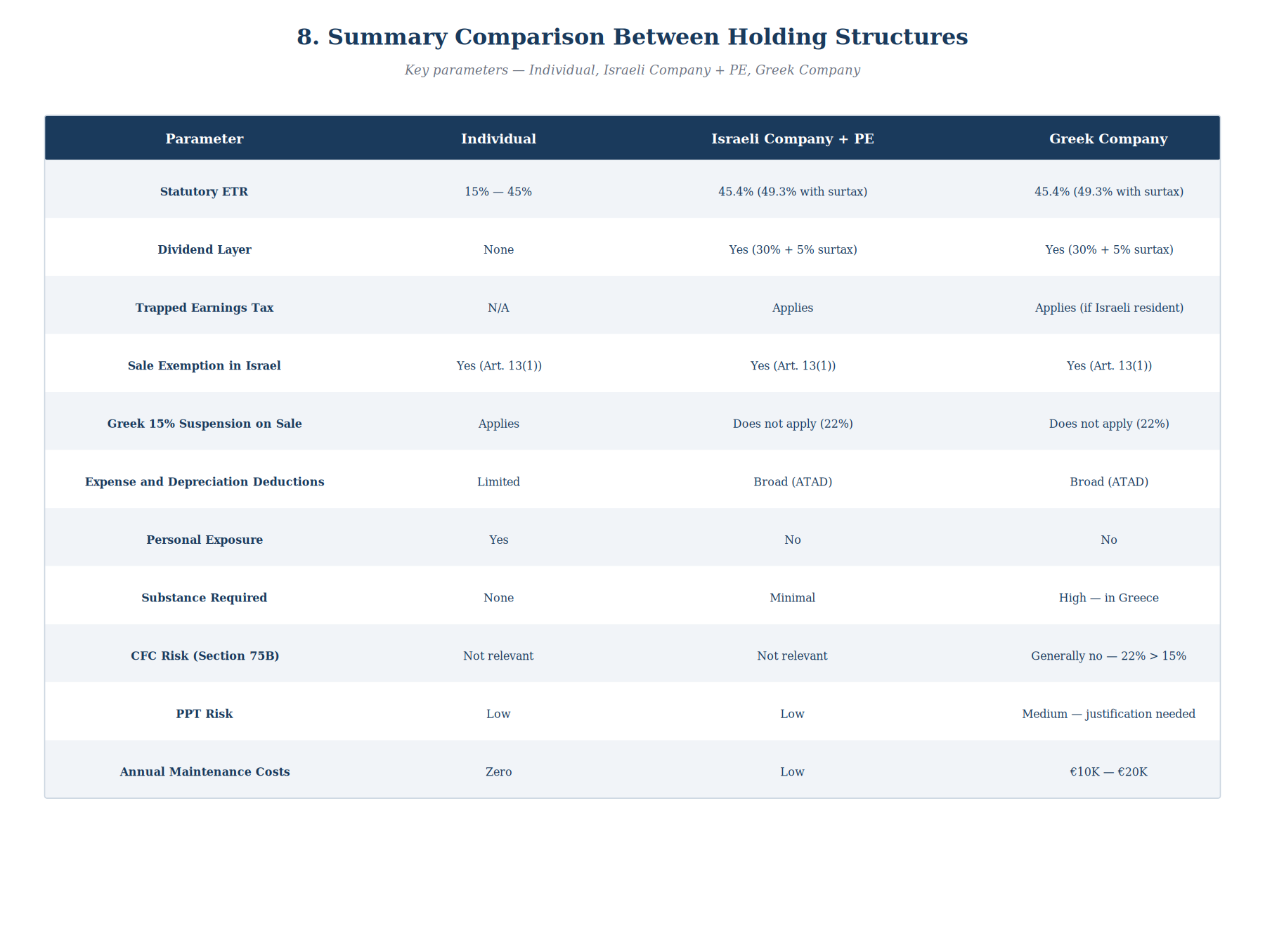

Summary Comparison

The following table summarizes the principal differences between the three holding structures across 11 parameters:

Conclusion

The tax picture of real estate investment in Greece is more complex than what emerges from a simple comparison of statutory tax rates. The common comparison between the 22% Greek corporate tax and the 45% maximum individual rate does not reflect the full picture — if only because it disregards the dividend layer that is added in a corporate structure. Conversely, a 45.4% statutory calculation in a corporate structure also does not necessarily reflect the realized burden — in practice, financing expenses, depreciation, operating expenses, and leverage materially reduce the Greek taxable base, and the actual effective rate may be substantially lower.

The choice of structure depends on numerous variables — the number of properties, projected income level, leverage, holding horizon, financial strategy, and additional issues such as CFC and PPT that arise in foreign holding structures. Each structure offers advantages and disadvantages in different domains — taxation, legal separation, flexibility on disposition, management centralization, and the ability to construct internal financing structures. In leveraged properties with substantial operating expenses, a corporate structure can offer a materially lower realized ETR. Each structure requires case-specific examination of the particular facts, and no single rule of thumb is appropriate for every situation.

This is general information only and does not constitute legal or tax advice. Data current as of May 2026.